How I Turned Charitable Giving Into a Smarter Inheritance Move

What if donating to charity could actually help your family keep more of your estate? I used to think charitable gifts were just about goodwill—until I learned how they can reduce tax burdens and reshape inheritance planning. As a beginner, I was overwhelmed, but small changes made a big difference. This is how I discovered a practical, tax-smart way to give back while protecting what I leave behind. It wasn’t about becoming a philanthropist overnight. It was about making thoughtful choices that aligned with my values and my family’s future. The more I learned, the clearer it became: charitable giving, when done strategically, isn’t just generous—it’s financially wise.

The Moment I Realized Giving Could Be Strategic

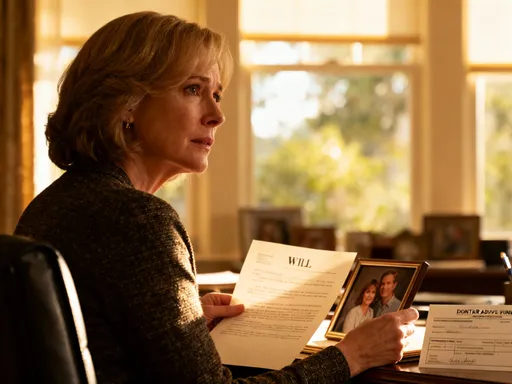

For most of my adult life, I saw charitable giving as something separate from financial planning. It was emotional, not analytical. I’d write checks to organizations I cared about—animal shelters, local food banks, educational programs—because it felt right. But I never considered how those gifts might fit into a larger picture, especially when it came to what would happen after I was gone. That changed when my aunt passed away. She had a modest estate—her home, a few investment accounts, and some personal savings. Nothing extravagant. Yet, her heirs faced a surprising tax bill. I didn’t understand it at first. How could someone with a relatively small estate owe so much? Then I learned about estate taxes and the way they’re calculated on the total value of assets before distribution. The lesson hit hard: without planning, even a well-intentioned estate can leave a financial burden on loved ones.

It was during a conversation with her estate attorney that I first heard the idea that charitable giving could be part of the solution. He explained that if my aunt had included charitable bequests in her will or made gifts during her lifetime, the taxable value of her estate could have been reduced. That meant less tax, more left for her heirs, and support for causes she cared about—all at once. At first, it felt strange to think of charity as a financial tool. It almost seemed to diminish the act of giving. But the more I reflected, the more I saw it differently. Strategic giving wasn’t about reducing generosity—it was about maximizing impact. It allowed me to honor my values while also being responsible to my family. This shift in perspective opened the door to a new way of thinking about wealth, legacy, and what it means to plan ahead.

Why Estate Taxes Hit Harder Than You Think

Many people assume estate taxes only affect the ultra-wealthy—billionaires, celebrities, or families with sprawling fortunes. That’s a common misconception. While it’s true that only estates above a certain threshold are subject to federal estate tax, that threshold isn’t as high as some might think, and it changes over time. More importantly, even if an estate doesn’t owe federal tax, state-level estate or inheritance taxes may still apply. For families with accumulated savings, home equity, retirement accounts, and investment portfolios, the total value can add up quickly—often enough to trigger tax liability. The key point is this: estate tax isn’t just about income. It’s about the total value of everything you own at the time of death, including real estate, life insurance proceeds, and retirement accounts.

The way the tax works is straightforward in theory but complex in practice. The government allows a certain amount to pass tax-free—the exemption amount—which, as of recent years, has been over $12 million for individuals, though this figure is subject to legislative changes. Any amount above that is taxed, sometimes at rates as high as 40 percent. But here’s what most people don’t realize: this tax is applied before assets are distributed to heirs. That means the estate itself pays the tax, often forcing the sale of assets to cover the bill. For families who inherit a home or a business, this can mean losing part of what was meant to be preserved. It’s not just about losing money—it’s about losing legacy. And because the tax is calculated on the gross estate, every dollar that can be legally removed from that total through planning can make a meaningful difference.

Another misconception is that estate planning is only for the elderly or the very rich. In reality, anyone who owns property, has retirement savings, or expects to leave behind assets should consider how those assets will be handled. Without a plan, state laws determine distribution, which may not align with personal wishes. More importantly, without strategies to reduce the taxable estate, heirs may receive less than expected—not because of poor management, but because of avoidable taxes. That’s why understanding the basics of estate taxation isn’t just for financial experts. It’s for anyone who wants to protect what they’ve worked for and ensure their loved ones are taken care of in the most efficient way possible.

Charitable Donations: More Than Just Goodwill

Charitable giving is often seen as a personal, emotional decision. And it should be. But it can also be one of the most effective tools in estate planning. When structured properly, donations to qualified charities can directly reduce the size of a taxable estate. This is because the value of the gift is subtracted from the total estate before taxes are calculated. For example, if an estate is worth $3 million and $500,000 is left to charity, the taxable estate becomes $2.5 million. That reduction can mean the difference between owing tax and staying below a threshold. It’s not about giving away wealth recklessly—it’s about using generosity as a strategy to preserve more for family while supporting meaningful causes.

There are two main ways charitable gifts impact estate taxes: lifetime giving and testamentary giving. Lifetime giving means donating while you’re still alive. This approach offers immediate tax benefits, such as income tax deductions in the year the gift is made, depending on the type of asset and the donor’s tax situation. It also allows the donor to see the impact of their gift and adjust their giving over time. Testamentary giving, on the other hand, happens through a will or trust. It doesn’t provide an income tax benefit during life, but it does reduce the estate’s value at death, lowering or eliminating estate tax. Both approaches have their place, and many people use a combination of the two to balance control, timing, and tax efficiency.

One of the most powerful aspects of charitable giving in estate planning is its flexibility. Unlike other estate planning tools that may require complex legal structures or irrevocable decisions, charitable gifts can be tailored to fit individual circumstances. You can designate a specific percentage of your estate to charity, name a charity as a beneficiary of a retirement account, or set up a trust that provides income to family members before distributing the remainder to a cause. The key is intentionality. Without a clear plan, assets may be distributed in ways that don’t reflect your values. But with thoughtful design, charitable giving becomes a bridge between personal legacy and financial responsibility.

How Donor-Advised Funds Changed My Game

When I first started exploring ways to make my giving more strategic, I came across donor-advised funds, or DAFs. At first, the term sounded intimidating—like something only financial advisors or wealthy donors would use. But once I understood how they work, I realized they were surprisingly accessible. A donor-advised fund is essentially a charitable investment account. You contribute cash, securities, or other assets to the fund and receive an immediate tax deduction. The money then grows tax-free over time. Later, you recommend grants from the fund to charities you support. The beauty of a DAF is that it separates the timing of the tax benefit from the timing of the giving. You get the deduction when you contribute, but you can take your time deciding exactly which organizations to support.

For me, this was a game-changer. I had been inconsistent with my giving—sometimes generous in good years, less so when expenses were high. With a DAF, I could make a larger contribution in a year when my income was higher, lock in the tax deduction, and then distribute the funds gradually over time. I also discovered that donating appreciated stocks or mutual funds to a DAF could be even more tax-efficient. Instead of selling the stock, paying capital gains tax, and then donating the after-tax amount, I could donate the stock directly. The full market value went into the DAF, I avoided capital gains tax, and I still got a deduction for the full value. It was a win-win: more money went to charity, and I kept more in my pocket.

Setting up a DAF was simpler than I expected. I worked with a major financial institution that offered DAF services, completed the paperwork online, and funded the account within a few weeks. There were no minimums that felt out of reach, and the administrative burden was minimal. The fund handled all the recordkeeping, compliance, and grant processing. I didn’t need to be an expert in tax law or investment management. I just needed to decide how much to contribute and which charities to support over time. Over the years, my DAF became a central part of my financial plan—a place where generosity and strategy came together in a practical, sustainable way.

Planning That Protects Both Family and Causes You Care About

One of the biggest concerns I had when starting this journey was balance. I wanted to support charitable causes, but I also wanted to make sure my family was taken care of. I didn’t want to feel like I was choosing between them. What I learned is that estate planning isn’t about choosing one over the other—it’s about designing a structure that honors both. By including charitable giving in my plan, I wasn’t taking away from my family. I was making the entire estate more efficient. Every dollar given to charity reduces the taxable estate, which means less tax is owed, and more can ultimately pass to heirs. It’s not a zero-sum game. It’s a way to stretch what I have further.

There are several ways to integrate charitable giving into an estate plan without compromising family security. One common method is to leave specific bequests in a will—such as a fixed amount or a percentage of the estate—to a charity. Another is to name a charity as a beneficiary of a retirement account, like an IRA or 401(k). This can be especially efficient because retirement accounts are fully taxable to heirs, but not to charities. So, by leaving a taxable account to a charity and other assets to family, you can optimize the after-tax value for everyone involved. Trusts can also be used to create more complex arrangements, such as a charitable remainder trust, which provides income to family members for a set period and then directs the remaining assets to a cause.

What makes this approach powerful is that it works at every level of wealth. You don’t need to be a millionaire to benefit. Even modest estates can see real advantages from intentional planning. For example, a couple with a $1.5 million estate might leave $150,000 to a charity they’ve supported for years. That reduces the taxable estate by 10 percent and ensures that a meaningful gift is made. At the same time, the rest of the estate passes to their children with less tax drag. It’s not about the size of the gift—it’s about the thought behind it. And when family members understand the reasoning, they often feel pride rather than concern. They see that the plan reflects values, not just numbers.

Common Mistakes Beginners Make (And How to Avoid Them)

When I first started learning about charitable estate planning, I made a few missteps. I assumed that writing a check to charity was enough. I didn’t realize that without proper documentation or integration into my overall plan, my wishes might not be honored. One of the most common mistakes is failing to communicate intentions. If your family doesn’t know about your charitable goals, they may not carry them out. Another error is overlooking the details of tax rules. Not all gifts qualify for deductions, and the rules vary depending on the type of asset, the timing, and the organization. For example, donating to a private foundation has different tax implications than giving to a public charity. Without understanding these differences, you could miss out on benefits or even trigger unintended consequences.

Another pitfall is waiting too long to act. Many people assume they can wait until they’re older to think about estate planning. But life is unpredictable. Starting early gives you more time to explore options, adjust your strategy, and take advantage of tax benefits while you’re still able to enjoy them. It also reduces stress for your family later. A related mistake is trying to do everything alone. While you don’t need to be a financial expert, working with a qualified advisor—such as an estate planner, tax professional, or financial consultant—can help you avoid costly errors. These professionals don’t have to manage your entire life, but they can provide clarity on complex rules and help you make informed decisions.

The good news is that you don’t have to get everything perfect right away. Start small. Open a DAF with a modest contribution. Update your will to include a charitable bequest. Talk to your family about your values. Review your plan every few years, especially after major life events like marriage, divorce, or the birth of a grandchild. The goal isn’t perfection—it’s progress. The most important thing is to begin. Every step you take makes your plan more resilient and your legacy more intentional.

Building a Legacy That Reflects Your Values—Without the Stress

Looking back, the biggest shift for me wasn’t just about saving money or reducing taxes. It was about seeing financial planning as an extension of my values. I used to think of money as something separate from meaning—a tool for security, not expression. But by integrating charitable giving into my estate plan, I realized that how I manage my finances can reflect what I believe in. My legacy isn’t just about what my family inherits. It’s about the impact I leave on the world. And the beautiful part is that these goals don’t have to compete. They can support each other.

Tax optimization often gets a bad reputation, as if it’s about finding loopholes or avoiding responsibility. But when used wisely, it’s the opposite. It’s about being responsible—responsible to your family, your community, and your own principles. By reducing unnecessary taxes, you preserve more for your heirs. By directing gifts to causes you care about, you extend your influence beyond your lifetime. And by planning ahead, you relieve your loved ones of difficult decisions during an emotional time. That’s not cleverness for its own sake. That’s stewardship.

You don’t have to overhaul your entire financial life to make a difference. Start with one step. Research donor-advised funds. Talk to an advisor about your estate. Update your beneficiary designations. Even a small change can set a new direction. The goal isn’t to become a financial expert overnight. It’s to make thoughtful choices that align with who you are and what you care about. In the end, the most lasting inheritance isn’t just money. It’s the example you set—the values you live by, the causes you support, and the care you show for both family and community. That’s a legacy worth planning for.